Schließen

SchließenSchnell durch die Krise – Sportmodelle sind trotz Pandemie und Klimawandel weiterhin gefragt. Zu welchen Tarifen, hat Schwacke ermittelt

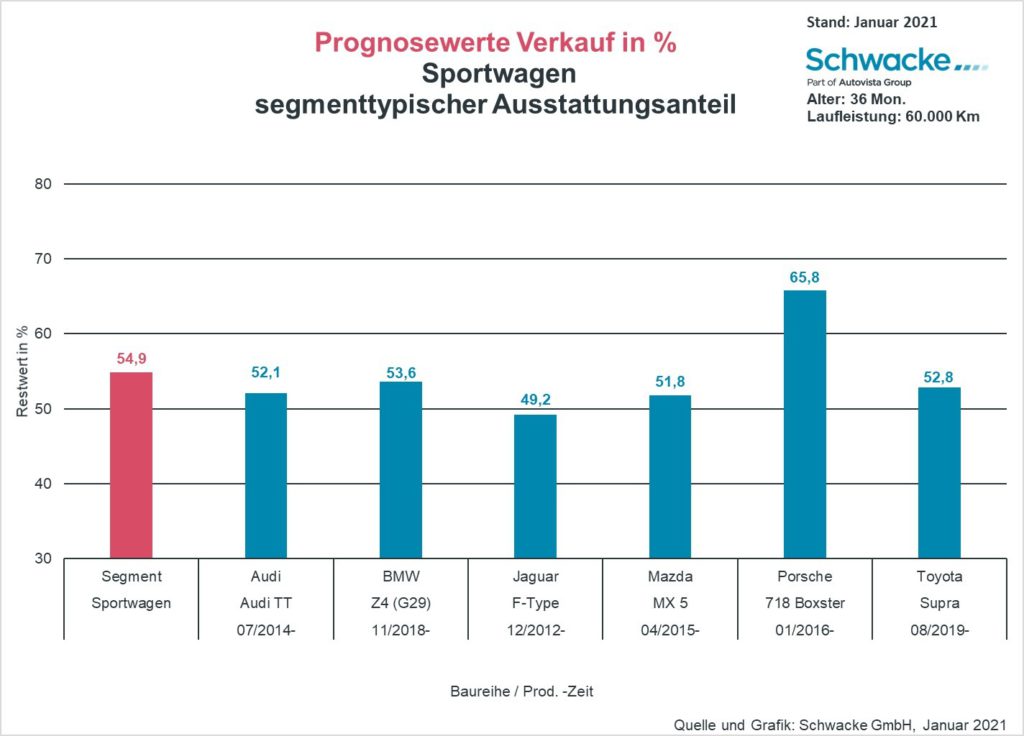

Sportmodelle erweisen sich in Krisensituationen meist als sehr robust im Vertriebssinne. So auch in der Pandemie. Zwar schaffen die relativ wenigen Modelle es nur selten über gering vierstellige Neuzulassungszahlen hinaus, aber das Kundeninteresse insbesondere bei hochmotorisierten und teuren Modellen ist ungebrochen – neu wie gebraucht. Am ehesten machen den Herstellern da noch Abgasnormen und CO2-Strafsteuern zu schaffen. Dies führte dazu, dass Versionen und Modelle wie zuletzt beispielsweise der Fiat 124 Spider oder der Import der Camaros und Corvettes eingestellt oder drastisch reduziert wurden. Zumal die Produzenten an CO2-stärkeren Benzinmotoren kaum vorbeikommen. Alternative Antriebe sind entsprechend noch selten. Eine große Ausnahme bildet hier der Porsche Taycan, der nicht nur in 2020 häufiger zugelassen wurde als alle Cayman und Boxster zusammen, sondern nach dem deutlich selteneren i8 auch die einzig relevante Neuentwicklung bei E-Sportlern überhaupt ist. Angesichts der relativ stabilen Restwert-Performance der Verbrenner und der im Verhältnis zu den Stückzahlen hohen Entwicklungskosten ist nachvollziehbar, dass sich hier kein so starker Elektroboom entwickelt wie in den anderen Fahrzeugsegmenten und die Hersteller sich zurückhalten. Vielleicht stellen auch die hochmotorisierten anderen Elektro-Bauformen das massentauglichere Konzept dar. Schließlich gibt es bereits einen Volvo XC40 der mit 408 elektrischen PS in unter 5 Sekunden auf 100km/h spurtet. Die hier gezeigten Verbrenner-Modelle wiederum decken segmenttypisch eine große Bandbreite ab an Preisen und Motorisierungen. Gerade das scheint Kunden die gewünschte Auswahl zu bieten, um sich mit jedem Geldbeutel einen Hingucker vor die Tür stellen zu können. Das lässt offenbar den Modellen ausreichend Spielraum und Zielgruppe für angemessene Wiederverkaufspreise. Auf Komfort muss dabei heute niemand mehr in einem Sportler verzichten. Längst stehen die meist zweisitzigen Sprinter einer Mittelklasse in puncto Serienausstattung und Aufpreisliste in kaum etwas nach. Besonders die jüngeren Jahrgänge zeigen rapide ansteigende Einbauraten an Infotainment, Sicherheitsfeatures und hochwertiger Beleuchtung. Das Segment hat also trotz aller Unkenrufe auch als Verbrenner Zukunft. Ein paar mehr elektrifizierte Varianten werden aber dennoch nicht lange auf sich warten lassen.