Schließen

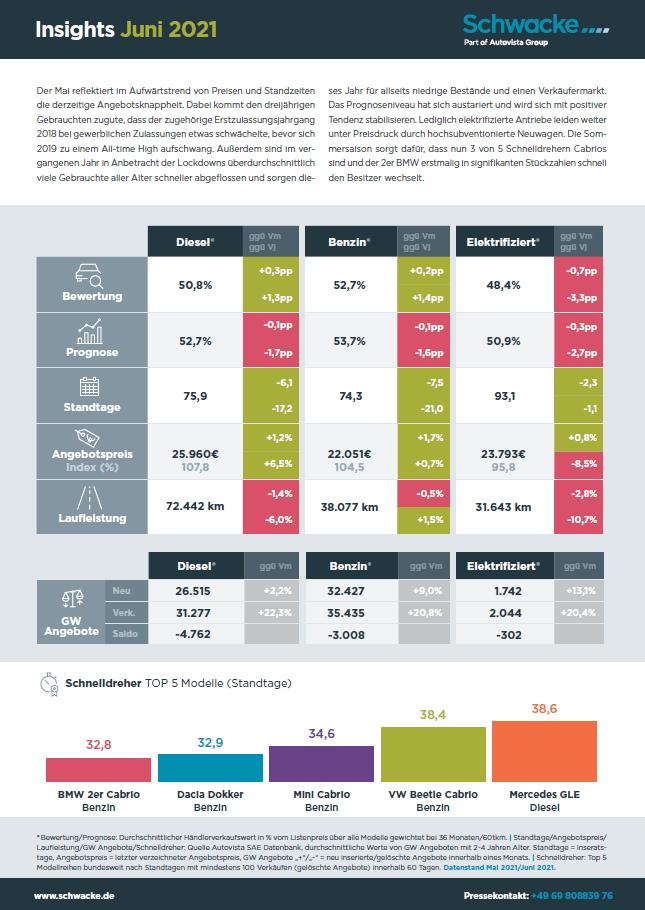

SchließenDer Mai reflektiert im Aufwärtstrend von Preisen und Standzeiten die derzeitige Angebotsknappheit. Dabei kommt den dreijährigen Gebrauchten zugute, dass der zugehörige Erstzulassungsjahrgang 2018 bei gewerblichen Zulassungen etwas schwächelte, bevor sich 2019 zu einem All-time High aufschwang. Außerdem sind im vergangenen Jahr in Anbetracht der Lockdowns überdurchschnittlich viele Gebrauchte aller Alter schneller abgeflossen und sorgen dieses Jahr für allseits niedrige Bestände und einen Verkäufermarkt. Das Prognoseniveau hat sich austariert und wird sich mit positiver Tendenz stabilisieren. Lediglich elektrifizierte Antriebe leiden weiter unter Preisdruck durch hochsubventionierte Neuwagen. Die Sommersaison sorgt dafür, dass nun 3 von 5 Schnelldrehern Cabrios sind und der 2er BMW erstmalig in signifikanten Stückzahlen schnell den Besitzer wechselt.