Schließen

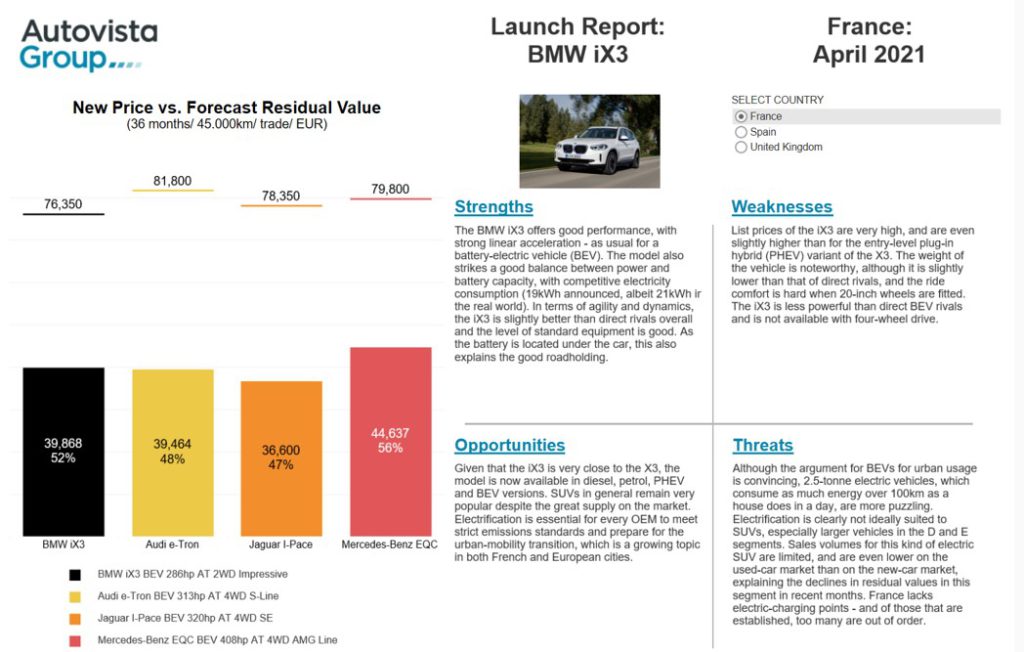

SchließenThe iX3 is BMW’s first pure-electric X model and is the most conventional, being effectively a battery-electric vehicle (BEV) version of the best-selling X3.

The iX3 offers good performance, with strong linear acceleration – as usual for a battery-electric vehicle (BEV). The model also strikes a good balance between power and battery capacity, with competitive electricity consumption. In terms of agility and dynamics, the iX3 is slightly better than its direct rivals overall. As the battery is located under the car, this also explains the good roadholding.

Standard equipment is comprehensive, including three-zone climate control, heated and powered front seats (with memory function on the driver’s side), BMW Teleservices and wireless phone charging. Safety features include emergency-assist and rear cross-traffic alert. The 458km range of the iX3 is second only to the Jaguar I-Pace’s 470km range, and it has the fastest charging time when connected to an 11kw AC wallbox, of 7.5 hours.

In addition to BMW’s strong brand image, the iX3 is supported by the company’s longer expertise in electrification. This started with the i3, which has been on the market since 2013, and was followed by plug-in hybrid (PHEV) engines offered on different models in the range, including one for the brand’s X family.

As the first conventional BEV from BMW, the iX3 compares well against key competitors. It is offered at an attractive entry price point and the popularity of both the brand and the X3 range should ensure plenty of demand. Given that the iX3 is very close to the X3, BMW’s D-SUV range is now available in diesel, petrol, PHEV and BEV versions.

Click here or on the image below to read Autovista Group’s benchmarking of the BMW iX3 in France, Spain and the UK. The interactive launch report presents new prices, forecast RVs and SWOT (strengths, weaknesses, opportunities and threats) analysis.