Schließen

SchließenThe latest edition of Autovista Group’s whitepaper: How will COVID-19 shape used-car markets? considers the third-wave of coronavirus infections across Europe, and looks at the lessons learned a year since the pandemic first hit the continent.

The whitepaper covers topics including:

- One year into COVID-19 and the lessons of resilience

- Used-car markets 2021 – crisis? What crisis?

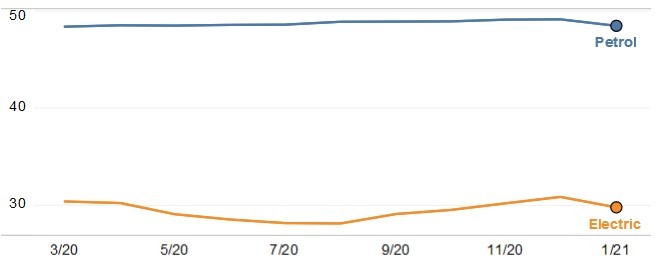

- Electric vehicle (EV) tax guide

- Europe’s used-car market forecasts for 2021 and 2022

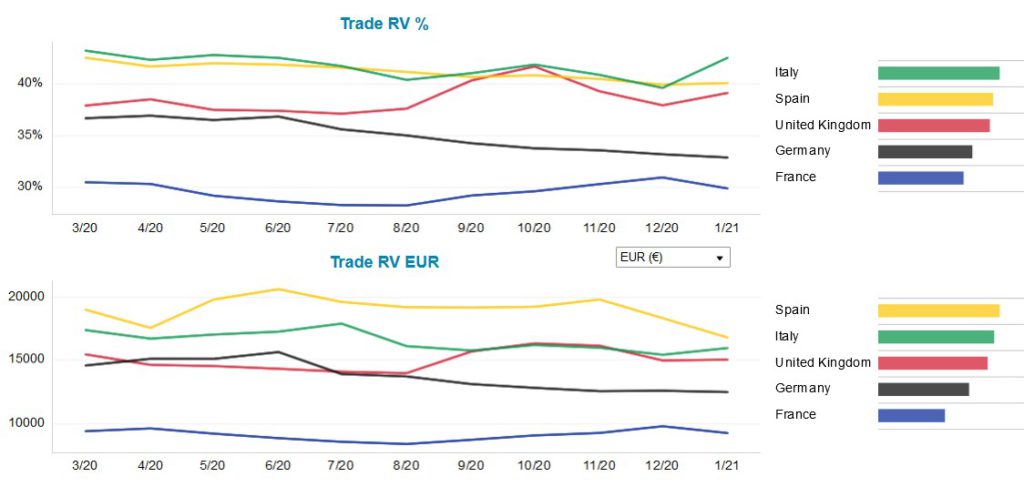

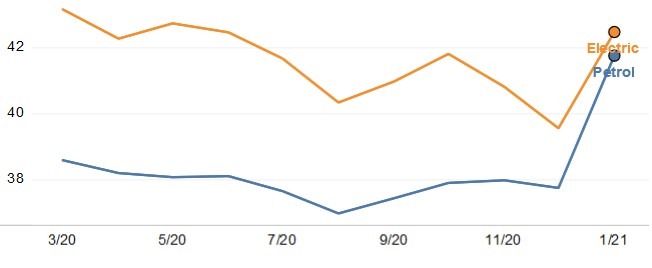

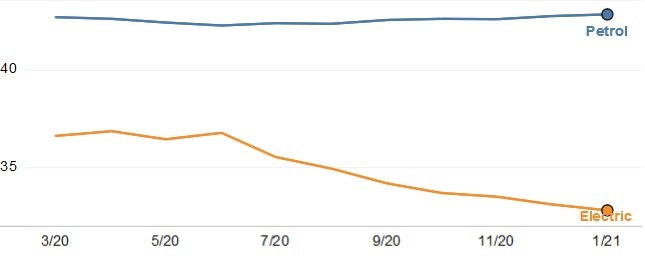

Following the emergence of Europe’s automotive sector from COVID-19 lockdowns, a three-speed development of residual values (RVs) has prevailed across the region. Autovista Group’s COVID-19 tracker, which covers 12 European markets, has revealed that residual value (RV) indices for a number of countries have returned to pre-crisis levels. Some, however, are still struggling.

Autovista Group experts discussed the whitepaper findings in the company’s latest webinar – Europe’s used-car markets – recovery from COVID-19. You can watch the presentation below.

Remaining strong

Used-car markets have proven more resilient than expected. In fact, the pandemic has helped some developments over the finish line that have long been in the making. For example, online sales, an advance that the automotive industry was slow to adopt until COVID-19 made it a necessity. Also supply-chain disruption has pushed demand towards the used-car sector.

In addition, the latest whitepaper looks at forecasts for RV development in Europe for 2021 and 2022. Autovista Group experts analyse the latest trends and scenarios for used-car market development across the continent. As countries are hit by a third-wave of infections, economic recovery may yet extend into 2022, even as vaccination programmes pick up their pace.

You can find more information about how different markets are shaping up, and the various economic scenarios across the region, in the latest update of the Autovista Group whitepaper – ‘How will COVID-19 shape used car markets’ – which can be viewed here.