Schließen

SchließenBMW is carrying out a global recall of some of its plug-in hybrids (PHEVs) produced this year, due to battery fire concerns. The carmaker is also suspending delivery of affected vehicles as part of a ‘preventative measure.’

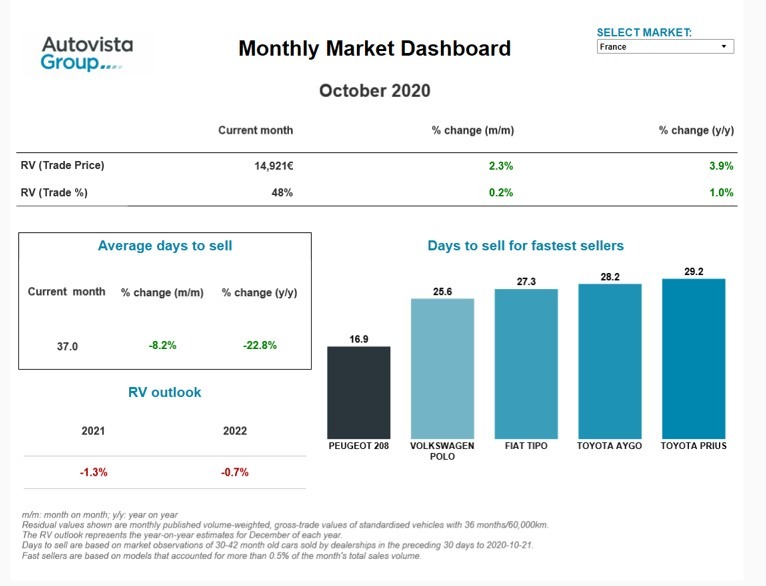

In the first of a new monthly initiative, Autovista Group has created a dashboard showcasing the latest data on residual values, average selling days, the fastest-selling used cars and the residual value outlook in France, Germany, Italy, Spain and the UK. Senior data journalist Neil King discusses the findings.

Autovista Group’s new monthly market dashboard (MMD) reveals that the average residual value (RV) of cars aged 36 months and with 60,000km grew year on year in all the Big 5 European markets in October. Even RV retention, represented as RV%, grew year on year in all markets except Germany. The highest growth in RV% terms was in the UK, where the average RV% was 48%, equating to a 1.9% improvement on September and a healthy 14.9% change compared to October 2019.

As reported in our coverage of the ‘three-speed’ development of RVs across Europe, the UK is enjoying the release of pent-up demand, both from the coronavirus (COVID-19) lockdown and the uncertainty running up to the country’s departure from the European Union on 31 January. The country also faces a starker vehicle-supply challenge than any other market, which is filtering through to higher RVs as used-car demand outstrips supply.

Quicker rehoming

In addition to the growth in RVs in most markets during October, three-year-old cars are also selling quicker than a year ago in all the major European markets, except Spain. Three-year-old cars are selling the quickest in the UK, moving on after an average of just 33 days. However, the greatest reduction in the average number of days for 36-month-old cars to sell, compared to October 2019, was in France. These vehicles now have to wait on average only 37 days to find a new buyer in France, sitting idle for a significant 23% fewer days than in October 2019.

The fastest-selling model in France in October 2020 was the Peugeot 208, which took just 17 days to find a new home. After the Peugeot 208 in France, the fastest-selling models across the major European markets were in the UK. The Range Rover Evoque and the Mercedes-Benz GLC also took less than 20 days to be rehomed in October.

The future’s not so bright

The new MMD also features the latest Autovista Group RV outlook for the major European markets. The current trend for rising RVs is unfortunately not forecast to continue in 2021. Autovista Group predicts that at year-end 2021, compared to year-end 2020, RVs of cars in the 36 month/60,000km scenario will be lower in France, Italy, and the UK and merely stable in Spain. The weakest outlook is for Italy, where RVs are currently forecast to be 3.9% lower by the end of 2021 than at the beginning of the year. RVs are only expected to be higher in Germany, albeit with year-on-year growth of only 0.4% forecast for both 2021 and 2022.

Click here or on the screenshot above to view the monthly market dashboard for October 2020.